Why Is the Cost of Owning a Home So High Now?

There has been growing concern about the affordability of homeownership in the United States, particularly for first-time homebuyers. The rapid rise in house prices during the pandemic has been followed by a steep increase in borrowing costs in 2022, with average 30-year fixed mortgage rates remaining above 6% since September of 2022.

Other costs have risen as well—higher prices of construction materials together with increasing damage from climate disasters have contributed to a significant increase in homeowner insurance premiums.

In this context, affordability challenges have increasingly spread beyond historically high-priced coastal cities such as San Francisco and New York to sunbelt cities and beyond.

The affordability of residential housing has declined markedly in the United States since 2022. The Federal Reserve Bank of Atlanta’s Home Ownership Affordability Monitor tracks the median-income household’s ability to cover the annual costs associated with owning the median-priced home in a given market. Costs include payments of principal and interest at current mortgage interest rates, property taxes, property insurance and private mortgage insurance.

If the annual cost of homeownership exceeds a 30 percent share of the annual median household income, homeownership is considered unaffordable. By this measure, homeownership has become increasingly unaffordable at the national level since the pandemic.

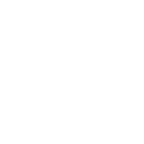

As of July 2025, the annual homeownership cost of a median-priced house in the United States took up 47% of median household income — exceeding prior peaks before the 2008 financial crisis (see chart below).

Chart: Courtesy of EconoFact

The problem of affordability has been spreading beyond traditionally high-priced cities. Housing markets vary greatly across locations and national averages can obscure important regional differences. The American Enterprise Institute has generated an affordability measure for first time homebuyers for the 60 largest metro areas in the country, based on the ratio of median house prices to median household income for the years 2013-2023. The top three most affordable metro areas are Pittsburgh, Cleveland, and Oklahoma City.

What is interesting is that the typical least affordable places to live—San Jose, San Francisco, and Los Angeles—were the top three metros in terms of the change in affordability between 2013 and 2023. That is, they became relatively more affordable because their real house price growth rates were below average over this period.

In contrast, the change in first-time homebuyer affordability has deteriorated the most since 2013 in cities like Boise City, Idaho; Dallas, Texas; Cape Coral and Deltona, Florida; and Grand Rapids, Michigan.

What has been driving the decline in affordability? The role that different factors have played in reducing homeownership affordability has varied over the past decade (see affordability drivers tab). Rising house prices have been a consistent driver in the decline in affordability, especially during the pandemic. Mortgage rates spiked after the Federal Reserve began to raise interest rates in March 2022 to counter inflation. The 30-year fixed rate mortgage reached a high of almost 7.8% in 2023, pricing homeownership beyond the reach of many households.

Although at a smaller scale, the cost of property insurance has also played a role in declining affordability more recently. Inflation and the rise in the cost of construction materials combined with more frequent damages from climate change have contributed to a significant increase in homeowner insurance premiums. The average home insurance premium in the United States rose by 33% from $1,902 in 2020 to $2,530 in 2023, according to a recent study.

One of the top reasons for the drop in affordability is related to housing supply. The lower the housing supply, the higher house prices will be. The United States faces a housing stock gap. While estimates of the shortfall vary, analysts agree that the available supply of housing in the United States has not been large enough to adequately meet existing demand.

Overall, the U.S. has been building fewer housing units relative to the number of households over the past three decades than historical trends with land use restrictions and local zoning as important limiting factors.

More recently, supply has also been limited by what is known as “mortgage lock-out.” Many homeowners have a mortgage with a low interest rate obtained before the Federal Reserve began raising the Federal Funds rate to combat inflation in 2022. These homeowners are reluctant to sell their house and give up their low-priced mortgage.

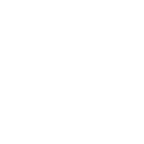

Furthermore, given the low supply of houses for sale, they are concerned that it will be difficult to find a new place to live and are reluctant to put their house on the market. Between 2015 and 2022 there was a sustained decrease in months of remaining housing supply, that is the number of months that it would take to sell the current inventory of homes at the current sales rate.

This decrease in inventory is consistent with a “sellers” market. But there has been a turnaround since 2022 and the number of months of remaining housing supply has since been trending up (see chart below).

Chart: Courtesy of EconoFact

Now that the Federal Reserve has started lowering the Federal Funds Rate, what should we expect in response from the housing market? The 30-year fixed mortgage rate is more closely tied to the 10-year Treasury Bill rate than the Federal Funds Rate, which is a short-term lending rate. Both the mortgage and Treasury bill rates appear to lead the Federal Funds rate by about 3 months.

This means that some of the expected decline in interest rates has already been priced in: Between July and September, both the 30-year fixed mortgage rate and the Treasury bill rate have fallen, likely in anticipation of the Fed lowering the Fed Funds rate.

Lower mortgage rates could relieve some of the “mortgage lock-out” effect, increasing housing supply on the market. They could also increase demand for housing, as more households become able to afford housing payments.

Historically, the 30-year real fixed mortgage rate and real house prices tend to move in opposite directions—a decrease in mortgage rates can increase demand for housing resulting in higher prices. But this has not been the case of late. The U.S. residential house price growth rate has been falling since 2024 and the real year-over-year real growth rate was negative in June 2025.

This decline is happening even though the 30-year fixed mortgage rate has been falling recently and was, on average, 6.17 percent on October 31, its lowest value in almost a year.

Of course, there is considerable heterogeneity across metro areas. Between the first quarter 2024 and second quarter 2025, 71% of the top 100 metro areas have seen positive real house price growth, whereas 29% have experienced negative growth.

For example, Detroit, Michigan and Rochester, New York experienced positive real house price growth rates, whereas Austin, Texas and Sarasota, Florida experienced negative growth. In fact, Austin and Sarasota sustained significant positive growth rates during the beginning of the 2020s, but then underwent significant declines.

What This Means

What can we expect from the housing market going forward? First, we might expect the 30-year fixed mortgage rate to fall in anticipation of further interest rate cuts by the Federal Reserve, but likely not by too much. House price growth rates are likely to continue to moderate.

But the impact on new housing supply is likely to be minimal. Rising costs of building materials due to increasing tariffs and the decline in construction workers due to new federal policy to deport undocumented immigrants has certainly generated headwinds for the construction industry.

The most important takeaway though, is that we are in unprecedented times. The U.S. housing market has shown a lot of variability recently, particularly since the start of the COVID pandemic in the spring of 2020. Federal immigration policy, tariffs, and climate change have added to the variability, adding to the uncertainty in any forecast of future market conditions.

Jeffrey Zabel is a professor in the Department of Economics at Tufts University.

This article was originally published on Econofact, a non-partisan publication designed to bring key facts and incisive analysis to the national debate on economic and social policies. EconoFact is overseen by Michael Klein, a professor of international economics at The Fletcher School.

- ‘I’m Doing Something Bigger Than Myself’A dentist and Army Reservist on selfless service in the military and civilian worlds

- $4 Million Gift to Advance Women’s HealthTufts Board Chair Jeff Moslow and Linda Moslow fund initiative uniting medicine and nutrition, with focus on menopause and longevity

- Study Identifies Which Patients Benefit Most From New Schizophrenia DrugBy tracking real-world responses, researcher found patterns that could help doctors match the right treatment to the right patient

- Boston Forward Sam Hauser, Delta Dental Support Program for VeteransFor every assist this season, the insurance provider will donate $25 to TUSDM Cares for Veterans

- What Mamdani’s Victory Says About Engaging Gen Z VotersHis campaign drew a surge of new voters, including young people. Will the youth vote help shape the 2026 midterms, too?

- The ‘Black Forager’ Nibbles the CampusAlexis Nikole Nelson, an expert on foraging, shares advice for safely eating foods found in the wild